You’ve done everything right. You saved the 20% deposit. You found the perfect family home in the suburbs or that sleek apartment on St Kilda Road. You’re earning a solid salary and you feel ready.

But when you sit down with the bank or plug your numbers into a basic online tool, the result is a shock: The bank is offering you $100,000 less than you expected.

What went wrong?

Many Melbourne homebuyers assume that their income is the only thing that matters. They think, “I earn $120k, surely I can borrow $700k?”

However, Australian lenders use complex, often opaque formulas to determine your “serviceability”—essentially, your ability to pay back a loan without hardship. In 2026, with tighter APRA lending standards and high interest rates, banks are more forensic than ever. Often, it’s the small, hidden details in your financial profile—the “ghost debts” you didn’t think mattered—that are silently dragging your numbers down.

The good news? Most of these anchors are fixable.

Here are the five hidden factors that might be killing your borrowing power, and exactly how you can fix them to get that “Approved” stamp.

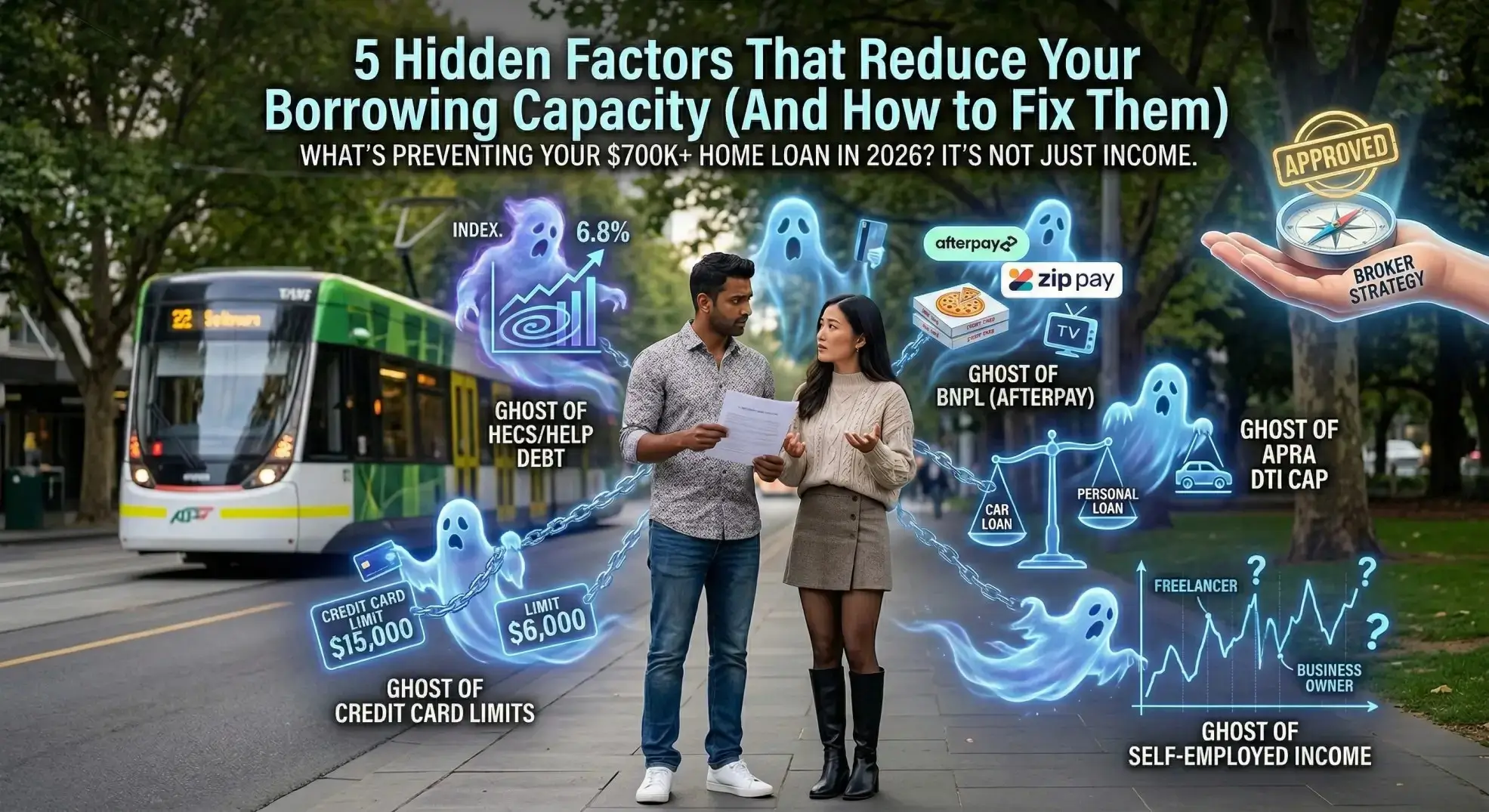

The “Ghost Debt” of Credit Cards

This is the single most common trap for first-home buyers and upgraders alike.

The Scenario: You have a credit card with a $15,000 limit. You rarely use it, or if you do, you pay the balance off in full every single month. You consider yourself to have $0 credit card debt.

The Bank’s Reality: The bank does not care that your balance is zero. They assess your application based on the limit.

Why? Because in the bank’s eyes, you could run out tomorrow, max out that card on a holiday or a shopping spree, and suddenly have a $15,000 debt with high monthly repayments. They must factor this potential liability into your “serviceability” calculation.

The Math

As a general rule of thumb, for every $10,000 limit on your credit card, your borrowing power is reduced by approximately $50,000.

- $6,000 Limit $\rightarrow$ Reduces borrowing power by approx. $30,000.

- $15,000 Limit $\rightarrow$ Reduces borrowing power by approx. $75,000.

The Fix:

Be ruthless. If you don’t need the card, close it. If you do need it, reduce the limit to the bare minimum (e.g., $1,000 or $2,000) at least one month before you apply for a loan. This simple email to your bank could unlock enough borrowing capacity to add an extra bedroom to your house hunt.

The New 2026 “Debt-to-Income” (DTI) Cap

In response to rising household debt, APRA (the banking regulator) has pushed lenders to tighten their “Debt-to-Income” (DTI) ratios. This is a silent killer for property investors or anyone with multiple existing loans and applies to 80% of the lender’s loans.

The Scenario: You earn a great income, but you also have a car loan, a personal loan for a renovation, and maybe a small investment property mortgage.

The Bank’s Reality: Many major lenders now have a “soft cap” on DTI at 6 times your income.

This means if your total household income is $150,000, your total allowable debt (including the new mortgage you want, plus your car loan, plus your HECS, plus your credit card limits) should not exceed $900,000.

If your existing debts already total $300,000, the bank may only lend you $600,000 for your new home—regardless of how much deposit you have or how easily you can afford the repayments.

The Fix:

You may need to consolidate smaller debts to clean up your ratio. Using a Finance Broker is crucial here, as we know which lenders have stricter DTI caps and which second-tier lenders have more generous policies for complex borrowers.

The “Netflix & Uber Eats” Effect (Living Expenses)

Gone are the days when banks just took your word for your living expenses. Today, thanks to Open Banking technology, Mortgage Brokers and some lenders can (and will) scour 3 to 6 months of your transaction history.

The Scenario: You earn good money, so you enjoy it. You have subscriptions to Netflix, Stan, and Spotify. You order Uber Eats three times a week. You have an Afterpay account that you use for clothes.

The Bank’s Reality: Lenders compare your declared expenses against the Household Expenditure Measure (HEM). If your actual spending is higher than the HEM benchmark, they will use your actual spending to calculate your loan.

- Buy Now, Pay Later (BNPL): Frequent use of Afterpay or Zip Pay signals to a credit assessor that you rely on debt for day-to-day living. This is a major red flag.

- Discretionary Spending: High spending on entertainment reduces your “Net Monthly Surplus,” which lowers the maximum loan amount you can service.

The Fix:

Go on a “Financial Detox” for 3 months before you apply.

- Cancel unused subscriptions.

- Cook at home instead of ordering in.

- Close all BNPL accounts.

This creates a “clean” paper trail showing the bank that you are a disciplined saver who can easily handle mortgage repayments. - Work with your Mortgage Broker to agree a realistic level of living costs that you can keep to, that will help you to borrow what you need.

The HECS/HELP Debt Indexation Blowout

Since the indexation rate spikes, HECS debt has moved from a background nuisance to a major borrowing blocker.

The Scenario: You have a $40,000 HECS debt. You think, “It’s just a small tax deduction, surely it doesn’t matter?”

The Bank’s Reality: It matters immensely. HECS repayments are deducted automatically from your salary, which lowers your Net Monthly Income.

If you earn $90,000 a year, your annual HECS repayment is around $5,000 to $6,000. That is $500 less per month in your pocket. To a bank, that $500/month “loss” reduces your borrowing capacity by roughly **$40,000 to $50,000**.

The Fix:

This is tricky.

- Option A: If your HECS balance is small (e.g., $5,000), it might be worth using part of your deposit to pay it off entirely to boost your borrowing power by $60k+.

- Option B: If the balance is large, paying it off might eat up too much of your deposit.

- Option C: Your Mortgage Broker can look at a few lenders who treat HECS more favourably if it can be repaid within 12 months

- Action: run the numbers on our Borrowing Power Calculator with and without the HECS debt to see the difference.

Inconsistent Income (The Self-Employed Trap)

If you are one of Melbourne’s many freelancers, contractors, or business owners, you know that cash flow isn’t always a straight line.

The Scenario: You made $100k profit last year, but you also had depreciation of $20k and the prior year was not so profitable. Total potential income available: $120k

The Bank’s Reality: Banks love stability. They hate fluctuation.

- If you are self-employed and have written off a lot of expenses to minimise your tax bill, the bank will look at your taxable income, which might be far lower than your actual cash flow.

- If your prior year was lower in profit, some banks will take an average of the 2 years profit plus addbacks. Some will only need to use the latest year – it can be confusing.

The Fix:

You need a Mortgage Broker that gets self-employed income. We know which lenders will accept the latest years figures and not look back over 2 years. We also understand which lenders are more generous on add backs such as depreciation. If all else fails, and your financials do not reflect the current trading position, we can look at Low Doc Loans for self-employed borrowers, allowing you to use BAS statements or accountant letters instead of tax returns.

The Verdict: Don’t Guess, Calculate.

Now that you know the “hidden anchors” holding you back, it’s time to see where you really stand.

Don’t rely on back-of-the-napkin math. Use our advanced Borrowing Power Calculator to test different scenarios.

- What happens if I close my $10k credit card?

- What if I pay off my car loan?

- How much can I borrow if I declare my real living expenses?

> Click Here to Calculate Your True Borrowing Power

Need a Strategy, Not Just a Loan?

Increasing your borrowing power is just step one. At Loanworx, we believe in structuring your finances so you don’t just get the loan—you get rid of it.

That’s why we created The Zero Debt Club.

It’s our exclusive program for clients that combines Certified Credit Coaches, personalised Debt-Deletion Strategies, and Disaster Plans to help you shave years off your mortgage and build true financial freedom.

Ready to get approved?

Book a no-obligation chat with our team today. We’ll review your unique situation, find the “ghost debts,” and help you present the strongest possible application to the right lender.